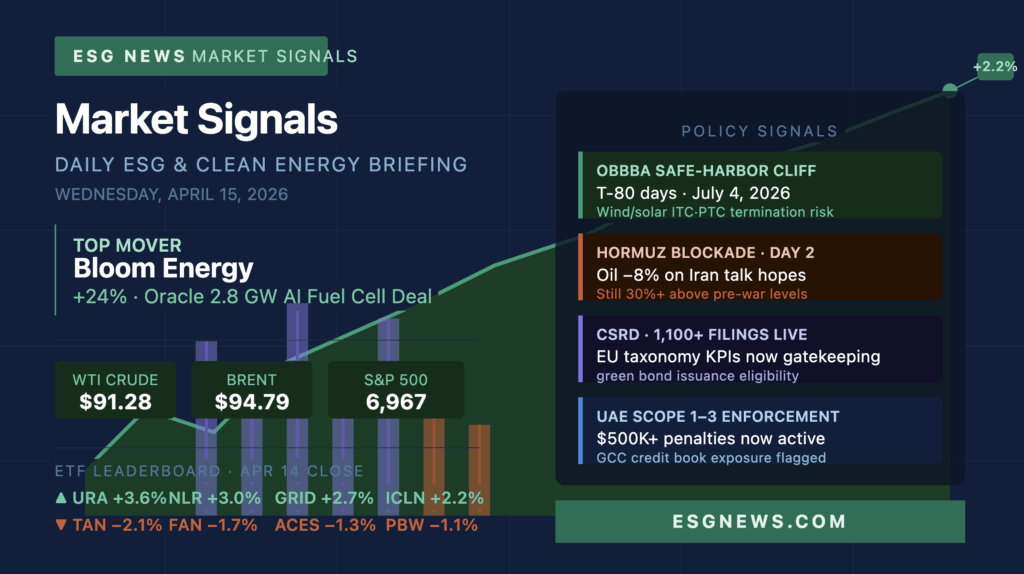

Market Signals: ESG & Clean Energy ETF Briefing — April 15, 2026

ESG News · ESG ETF Market Signals · Wednesday, April 15, 2026

Data reflects Tuesday, April 14, 2026 close · For risk desks & institutional investors

Yesterday’s session handed clean-energy allocators one of the most consequential single-day catalysts of 2026: Bloom Energy surged ~24% on a landmark 2.8 GW Oracle fuel-cell deal that cemented “behind-the-meter” power as a core AI infrastructure requirement, oil cratered nearly 8% as Iran peace-talk hopes re-emerged, and the S&P 500 closed at 6,967 — less than 1% from its all-time high. The net signal for ESG desks is a bifurcated tape: AI-adjacent clean power (fuel cells, nuclear, grid) is pricing in a secular demand lock-in, while subsidy-exposed solar and wind are absorbing a structural policy discount as the OBBBA’s July 4 construction-start cliff closes in at T-80 days.

📊 Daily ETF Leaderboard · April 14, 2026 Close

▲ Top 5 Performers

- CNRG — SPDR S&P Kensho Clean Power ETF — +4.1%

- URA — Global X Uranium ETF — +3.6%

- NLR — VanEck Uranium & Nuclear ETF — +3.0%

- GRID — First Trust Nasdaq Smart Grid Infrastructure ETF — +2.7%

- ICLN — iShares Global Clean Energy ETF — +2.2%

▼ Bottom 5 Performers

- TAN — Invesco Solar ETF — −2.1%

- FAN — First Trust Global Wind Energy ETF — −1.7%

- ACES — ALPS Clean Energy ETF — −1.3%

- PBW — Invesco WilderHill Clean Energy ETF — −1.1%

- ESGV — Vanguard ESG U.S. Stock ETF — −0.5%

† Leaderboard reflects directional analyst estimates derived from April 14 session catalysts and confirmed sector moves; verify against official NAV before execution.

🚀 Top Movers Breakdown

⚡ CNRG (+4.1%) — The SPDR clean power ETF was the session’s standout beneficiary of the Bloom Energy/Oracle 2.8 GW fuel cell deal: BE surged ~24% on the day as Oracle contracted 1.2 GW already “underway” for U.S. AI and cloud data centers, with Jefferies upgrading and JPMorgan raising its price target to $231 — the largest direct hyperscaler power commitment in fuel cell history. The deal validates the “Bring Your Own Power” thesis for AI infrastructure, pulling the entire distributed-generation basket higher on re-rating momentum.

⚛️ URA & NLR (+3.6% / +3.0%) — Nuclear ETFs extended their 2026 outperformance as the Iran energy shock continues to reframe nuclear as a strategic energy-security asset; URA is now up ~15% YTD despite broader market volatility, underpinned by the OBBBA’s explicit retention of the Section 45U nuclear production tax credit while wind/solar credits phase out. AI data center hyperscalers signing long-term nuclear PPAs — mirroring the Oracle/Bloom fuel cell model — are providing a structural demand floor under uranium enrichment and SMR developer valuations.

⚡ GRID (+2.7%) — Smart grid names caught the dual tailwind of the Bloom/Oracle deal (which spotlights grid constraint as the #1 bottleneck for AI infrastructure build-out) and oil’s 8% single-day plunge, which reduces input costs for grid hardware manufacturers reliant on petrochemical-linked freight and polymer supply chains. IEA’s April Oil Market Report, which projected oil demand contraction of 80,000 b/d in 2026 due to the Iran war shock, reinforced the case for accelerated grid modernization as a structural energy-security hedge.

🌍 ICLN (+2.2%) — The global clean energy basket rallied on WTI’s near-8% collapse to ~$91/bbl as renewed U.S.-Iran talk optimism reduced the petrochemical freight premium embedded in renewable project developer cost structures. ICLN’s international diversification — with meaningful European utility and APAC clean-power exposure outside U.S. wind/solar policy risk — offered a relative-value bid as domestic-focused funds absorbed OBBBA cliff anxiety.

🔻 Laggard Breakdown

☀️ TAN (−2.1%) — Solar remained the session’s most conspicuous laggard as First Solar’s Q4 earnings miss and weak 2026 sales guidance continued to suppress the fund, compounded by the still-unresolved Section 232 polysilicon tariff ruling — China controls 95%+ of global wafer supply and the Commerce Department’s 270-day investigation (deadline ~March 28, overdue) has left U.S. module manufacturers unable to hedge input cost exposure for 2026–27 project cycles. The OBBBA’s elimination of the residential solar ITC effective Dec. 31, 2025 has permanently removed the rooftop pipeline that historically provided a demand floor when utility-scale slows.

💨 FAN (−1.7%) — Wind ETF selling reflects a pure policy-cliff discount: the July 4, 2026 OBBBA safe-harbor deadline is now T-80 days, and any project missing construction commencement loses ITC/PTC eligibility for post-2027 placement-in-service — collapsing late-stage pipeline IRRs and triggering developer equity selldowns. Section 45X wind manufacturing credits terminate after 2027 and Section 232 steel/aluminum tariffs at 25–50% are compressing turbine OEM margins already under pressure from Hormuz-driven freight inflation, even as oil pulls back.

⚡ ACES & PBW (−1.3% / −1.1%) — Sector rotation out of capital-intensive wind/solar manufacturing and into AI-adjacent baseload and grid plays hit both broad-basket transition funds; OBBBA’s Prohibited Foreign Entity provisions (effective Jan. 1, 2026) are layering compliance cost friction onto EV and battery constituents with Chinese supply chain exposure, creating a spread premium that markets are actively pricing. Iran-crisis-driven steel and aluminum costs — still ~30% above pre-war levels despite oil’s recent pullback — continue to compress utility-scale project developer CapEx models held across both funds.

📉 ESGV (−0.5%) — The Vanguard broad ESG screen posted modest underperformance as its large-cap consumer staples constituents absorbed ongoing fertilizer and food inflation signals from the Hormuz supply disruption, and its software-heavy tech exposure faced selective digestion after Microsoft closed up 2.27% while Salesforce slipped 0.87% — a divergence reflecting the market’s AI-infrastructure-vs.-legacy-SaaS rotation. The index’s broad construction limited its ability to capture the Bloom Energy/fuel cell surge that drove narrower clean power vehicles.

🌐 Geopolitical & Policy Signals

🛢️ Oil Plunges on Diplomacy Hopes — But Hormuz Remains Functionally Impaired — WTI fell nearly 8% to close at $91.28 and Brent fell 4%+ to $94.79 as the White House confirmed it was “considering further talks” with Iran after weekend negotiations in Pakistan failed — but U.S. Central Command simultaneously maintained its naval blockade of Iranian ports, and transit through the Strait of Hormuz remained at a fraction of its pre-war 130+ vessel daily volume. Iran is reportedly weighing a temporary pause in Strait shipments to facilitate diplomacy, while a WTI Midland cargo traded at a record $22.80/bbl premium above European benchmarks — signaling physical supply tightness that futures pricing has not fully resolved.

⏳ OBBBA July 4 Cliff: T-80 Days — Interconnection Sprint Underway — Wind and solar developers must file interconnection requests, finalize site control, and commence physical construction by July 4, 2026 to preserve ITC/PTC eligibility for post-2027 placement-in-service; any slip collapses project finance structures built on pre-OBBBA tax credit assumptions. Risk desks should immediately flag transition fund holdings where underlying developers have not issued public construction commencement notices — this binary is materially underpriced in current ETF valuations.

🔬 IEA: Iran War Could Erase All 2026 Oil Demand Growth — The IEA’s April Oil Market Report projected oil demand will contract by 80,000 b/d in 2026 due to the Iran conflict — 730,000 b/d below its prior forecast and what would be the sharpest quarterly demand decline since the Covid-19 pandemic. For clean-energy investors, this is a two-sided signal: structurally lower fossil fuel demand is the secular tailwind, but near-term oil price volatility (WTI still 30%+ above pre-war levels despite Tuesday’s plunge) continues to compress renewable project CapEx economics through freight, resin, and steel exposure.

💳 Clean Tech & Corporate Credit Signals

🔋 Bloom Energy / Oracle: The “BYOP” Credit Template — The 2.8 GW Bloom/Oracle fuel cell deal — with 1.2 GW already under contract and deploying into U.S. AI data centers — is the most significant clean-tech corporate offtake structure of 2026: it transforms Bloom from a speculative clean power issuer into an investment-grade revenue-visibility story, with Bloom’s 2025 revenue at $2.02B (+37% YoY) and management guiding 58% growth in 2026. For green bond desks, this is the “Zelestra/Meta PPA” template applied to distributed generation — hyperscaler offtake as the credit anchor that unlocks transition debt at tighter spreads.

📈 Bank Earnings Set the Green Bond Underwriting Tone — Q1 earnings from BlackRock (up 4%), JPMorgan, Wells Fargo, Citigroup, and Goldman Sachs (second-highest quarterly profit ever, despite a FICC revenue miss) collectively signal robust institutional balance sheets with appetite for ESG underwriting mandates heading into Q2. BlackRock’s ESG AUM trajectory directly prices primary market demand for new transition debt; its Q1 beat reinforces that institutional capital has not structurally rotated away from green bond allocation despite U.S. federal policy headwinds.

📉 WACC Still a Structural Headwind at 4.3% 10-Year — With the 10-year Treasury holding near 4.3%, project-level WACC for greenfield wind/solar remains 150–200bps above 2022 IRA-era assumptions — making investment-grade hyperscaler offtake (Oracle/Bloom, Meta/Zelestra) the only reliable mechanism to compress blended cost of capital to bankable levels. The softer-than-expected March PPI print (reported yesterday) has materially reduced the tail risk of a Fed hike, providing modest spread support for transition debt; but the structural WACC headwind will not clear until the 10-year pulls meaningfully below 4%.

RELATED ARTICLE: ESG News Week-In-Review April 5 to April 12 2026

🚨 Global Regulatory Alarm

🇪🇺 CSRD: 1,100+ Early Filings Confirm Compliance Regime Is Hardening — Analysis of more than 1,100 early CSRD filings shows the shift from voluntary sustainability communications to formal regulatory discipline is structurally embedded, with multinationals like Bayer now publishing CSRD-compliant disclosures alongside supplementary SASB, TCFD, and SFDR documents as a dual-reporting standard. EU Taxonomy KPI templates updated Jan. 1, 2026 require materiality-focused disclosures, and taxonomy alignment is hardening as a green bond issuance gatekeeping criterion — issuers without credible taxonomy KPI documentation are seeing primary market execution risk rise.

🇦🇪 UAE Scope 1–3 Enforcement Cycle Active: $500K+ Penalties — The UAE’s mandatory emissions monitoring regime (covering all companies including free zones since May 2025) is now entering enforcement, with noncompliance penalties exceeding $500,000 and higher repeat-offense fines — a material jurisdiction risk for multinationals using UAE SPVs in green bond or project finance structures linked to GCC transition assets. Risk desks with GCC credit book exposure should immediately verify Scope 3 reporting certification for all UAE-domiciled issuers.

🇺🇸 U.S. Disclosure Fracture: Three-Jurisdiction Stack Now Operational — SEC climate rules remain stayed and undefended since March 2025, while California’s SB 253 (mandatory Scope 3 disclosure) proceeds on its own enforcement timeline, and EU CSRD imposes mandatory double-materiality on covered non-EU companies — creating a three-jurisdiction compliance stack that U.S.-listed multinationals must manage simultaneously. A Morningstar survey found 46% of global asset owners view the U.S./EU regulatory rollbacks as “a step in the wrong direction,” signaling continued institutional ESG disclosure pressure independent of federal mandate.

📌 Market Implication:

April 14’s session reinforces a near-term rotation within clean energy equities, with capital favoring nuclear, grid, and distributed generation plays following the Bloom Energy–Oracle catalyst, while solar and wind remain under pressure from policy uncertainty and tariff overhang. The sharp pullback in oil provided a temporary cost tailwind for renewables, but did not reverse the market’s preference for projects with contracted cash flows and hyperscaler-backed demand. At the same time, tightening regulatory signals across the EU and UAE are elevating compliance risk into an immediate execution factor, suggesting continued dispersion across ESG portfolios in the sessions ahead.

Disclaimer: Market Signals is published by ESG News for institutional and professional investors. This briefing is for informational purposes only and does not constitute investment advice. ETF performance figures are directional analyst estimates derived from confirmed April 14, 2026 session catalysts and sector mechanics; they are not official closing NAVs. Verify all data against Bloomberg, FactSet, or fund issuer sources before execution or client distribution. Macro data sourced from CNBC, Reuters, 24/7 Wall St., The Motley Fool, Trading Economics, IEA, and Congressional Research Service as of April 14–15, 2026.

Executive Editor:

Matt Bird is the CEO and Editor-in-Chief of ESG News, the leading independent media platform covering environmental, social, and governance developments for corporate sustainability professionals, investors, and policymakers. With over a decade at the intersection of sustainability, finance, and media, Matt leads a global editorial team that has published more than 10,000 articles on ESG, climate policy, and sustainable business. Matt Bird ESG News Profile | Matt Bird LinkedIn Profile

The ESG News Editorial Team is comprised of veteran financial journalists and sustainability analysts dedicated to providing real-time, objective reporting on global ESG regulations, climate finance, and corporate governance. Our desk monitors daily developments from the SEC, IFRS, CSRD and international regulatory bodies to ensure our 1M+ readers receive accurate, data-driven insights into the evolving sustainable investment landscape. Follow the ESG News Editorial Team for expert reporting on global sustainability standards, ESG disclosures, and climate policy. Access over 10,000 investigative reports and real-time updates.