SEC Moves To Rescind Corporate Climate Reporting Rules

- The SEC has formally proposed rescinding its 2024 corporate climate disclosure rules in full.

- The rules would have required public companies to disclose climate risks, severe weather impacts and, in some cases, greenhouse gas emissions.

- The proposal opens a 60-day comment period and is likely to face legal challenges from investor and environmental groups.

SEC Reverses Course On Climate Disclosure

Washington, D.C. regulators have opened a new front in the U.S. debate over climate risk, corporate reporting and investor protection.

The U.S. Securities and Exchange Commission has formally proposed rescinding its corporate climate disclosure rules. The rules were adopted in 2024 under former SEC Chair Gary Gensler. They would have created the first federal climate reporting requirements for U.S. public companies.

The proposal now moves the agency toward a full rollback. It also places the SEC back at the center of a legal and political fight over how much climate information investors should receive from listed companies.

The 2024 rules required companies to disclose climate-related risks that could affect their business. They also covered plans to manage those risks, the financial impact of severe weather events and, in some cases, greenhouse gas emissions from company operations.

For investors, the rules aimed to create more consistent reporting across public markets. For many companies, they added new compliance duties at a time of rising scrutiny over climate risk, energy policy and capital costs.

SEC Says Rules Exceed Its Authority

The SEC said the climate disclosure rules exceed the scope of its statutory authority. It also argued that the rules carry policy problems, even if the agency had authority to adopt them.

The Commission said the proposal is part of a return to a “materiality-focused approach to securities regulation.” It also said the rules impose significant costs on public companies and shareholders.

The agency argued that the rules are unnecessary under a registrant-specific approach to disclosure. It said they move beyond the policy concerns of federal securities laws. The SEC also said the rules conflict with its objectives of supporting capital formation and encouraging companies to remain public.

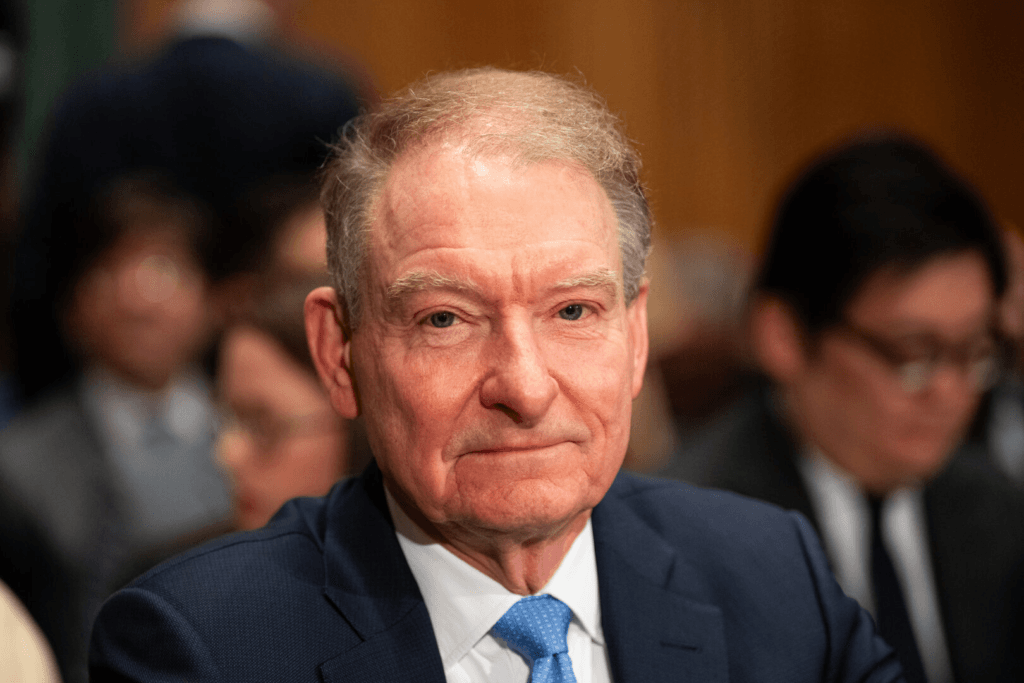

SEC Chair Paul Atkins said: “We must re-examine the costs, burdens, and benefits of disclosure mandates to make becoming and remaining a public company more attractive again. SEC disclosure obligations should comply with the Commission’s statutory authority, be guided by materiality as the North Star, avoid the practical effect of dictating corporate behavior, and be imposed only when the expected benefits justify the likely costs and burdens.”

His position reflects a broader shift in regulatory priorities under the Trump administration. The SEC first sought to stop defending the rules in court. It later asked the court to decide the issue without further agency reconsideration.

The U.S. Court of Appeals for the Eighth Circuit rejected that path in September 2025. The court said: “It is the agency’s responsibility to determine whether its Final Rules will be rescinded, repealed, modified, or defended in litigation.”

The SEC has now chosen the formal rulemaking route.

RELATED ARTICLE: SEC Moves To Scrap Biden Climate Disclosure Rule As Companies Face Patchwork Reporting Risk

Investors Face A New Disclosure Gap

The decision reopens a central question for boards and investors: when does climate risk become material financial information?

Supporters of the original rules argue that climate-related risks already affect asset values, insurance costs, supply chains and capital allocation. They also say voluntary reporting has created uneven data across sectors.

Environmental groups criticized the SEC’s move, especially its claim that the rules were not designed to provide material information to investors.

Kathy Fallon, Director, Land Systems at Clean Air Task Force, said: “The SEC’s mission is to protect investors and the public by ensuring they have access to material information. While imperfect, the rule was an important step toward giving investors consistent information about financially material climate risks, including the use of carbon offsets. “The Commission should withdraw this proposal and focus instead on implementing disclosure requirements that give both investors and the public the transparency they need.”

The rescission process could take months. The public comment period will remain open for 60 days after publication in the Federal Register. SEC staff must then review major issues raised during the comment period before any final rule can move forward.

Any final rescission could also face court challenges.

Legal Fight Likely To Continue

The Environmental Defense Fund has already said it will oppose the rollback. It argued that removing the rules could weaken protections for workers and retirees with savings invested in public markets.

Stephanie Jones, Senior Attorney for EDF, said: “Climate change is causing stronger, more frequent – and more expensive – weather disasters. That’s putting Americans’ money at risk along with their health and safety. At the same time, clean energy companies are innovating, creating jobs, and saving Americans money. The SEC’s Climate Risk Disclosure Rule makes sure people have information that they need to make important financial decisions.”

For companies, the proposal may reduce near-term federal reporting pressure. Yet it does not remove climate disclosure demands from global markets.

Large multinationals still face rising reporting expectations in Europe, California and other jurisdictions. Investors also continue to ask for decision-useful climate data, especially in sectors exposed to transition risk, physical risk and energy policy shifts.

The SEC’s move may ease one U.S. compliance burden. But it also deepens regulatory fragmentation. Global companies could now face wider gaps between U.S. federal reporting rules and disclosure regimes in other major markets.

For the C-suite, the takeaway is practical. Climate reporting may become less prescriptive at the federal level, but climate risk has not left the balance sheet. Boards will still need to decide what investors need to know, where risks are financially material and how disclosure aligns with capital strategy.

The U.S. rollback will be watched far beyond Washington. It could shape how other markets balance investor protection, political pressure and the cost of corporate climate transparency.

The ESG News Editorial Team is comprised of veteran financial journalists and sustainability analysts dedicated to providing real-time, objective reporting on global ESG regulations, climate finance, and corporate governance. Our desk monitors daily developments from the SEC, IFRS, CSRD and international regulatory bodies to ensure our 1M+ readers receive accurate, data-driven insights into the evolving sustainable investment landscape. Follow the ESG News Editorial Team for expert reporting on global sustainability standards, ESG disclosures, and climate policy. Access over 10,000 investigative reports and real-time updates.