The Super El Niño Is Coming. What Does That Mean for Crops?

Author: Will Kletter, COO ClimateAi

In 2023/24, El Niño wiped 14% off the global cocoa supply. Prices hit record highs. Procurement teams scrambled. And while that was a strong El Niño, the fifth strongest on record, it was not a Super El Niño.

ClimateAI’s latest El Niño outlook now assigns greater than 90% odds for El Niño conditions to start in 2026. Models are increasingly converging on a Super El Niño event, roughly six times the warming needed to qualify as an El Niño event.

Our models are already showing early signs of how this super El Niño could bring another supply shock to cocoa supply chains. With an 87% likelihood of high heat damage to disruption yields in the world’s third-largest producer, Indonesia, and a 71% likelihood of medium heat-damage risk in Ghana, the second-largest.

For most other crops, the 2026/27 growing season hasn’t started yet, but the signals are already there. For agricultural buyers, producers, and companies across the agricultural value chain, the question isn’t whether this will affect your sourcing. It’s whether you can act on it in time to mitigate losses.

What Makes 2026 Different from Other El Niños

A typical El Niño is defined by a 0.5°C warming of Pacific surface temperatures. What’s coming in 2026 could exceed 3.0°C. These types of temperature swings are the difference between a difficult growing season and global supply shocks and local famines.

The last Super El Niño in 2015, for example, led to corn and bean yield losses exceeding 90% in parts of Central America and contributed to the worst drought Ethiopia had seen in decades.

Many of the indicators used to monitor El Niño intensity are already flashing warning signs that this could be even worse. Subsurface Pacific temperatures have risen to +8°C at depths of 100–150 meters, surpassing levels observed at the same stage in the 1997 and 2015 Super El Niño events.

Another unusual, positive aspect of this El Niño is the amount of lead time agricultural supply chains still have to prepare. The El Niño Southern Oscillation (ENSO) can increase forecastability in certain areas where the relationships between the oceanic variables described above and outcomes on land are well known. As a result, ClimateAi’s models and others show a high degree of certainty about the Super El Niño threshold months inadvance. In practical terms, this means companies have unusually high confidence unusually early, allowing them to make contingency plans and adapt.

What the Early Signals Already Show

ClimateAi’s ENSO forecast for June, July, and August

RELATED ARTICLE: Mars Invests $5M to Protect Peanut Supply, Breed More Climate Resilient Crops

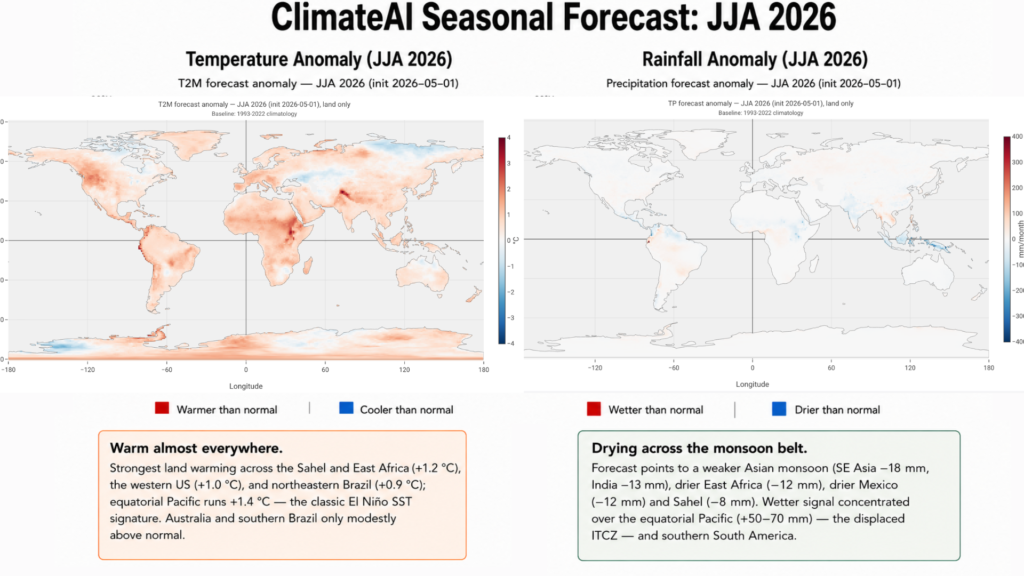

El Niño does not affect every region equally. Historically, it has been associated with hotter and drier conditions across Australia, Southeast Asia, India, Southern Africa, and parts of Central America, while bringing wetter conditions to western South America and the southern United States.

El Niño conditions are expected to strengthen through the second half of 2026, peak by the end of the year, and continue to influence global weather patterns well into 2027. Agricultural impacts could begin to emerge before the 2026 harvests and intensify through the 2027 growing season as shifts in rainfall and temperature patterns affect critical phases, such as planting, pollination, and grain fill.

Cocoa is the most visible signal we have right now, but we’ve seen this story before. During the last El Niño, global-mean crop yields for wheat, rice, and maize were down in critical growing regions. Heat and drought stress during the 2026/27 growing cycle are likely to exceed what producers experienced during the last El Niño. Especially in Australia, Southeast Asia, and parts of Africa, which have been historically hammered by El Niño-driven droughts. Where crops like rice, maize, and wheat are staple crops for most of the population.

The first warning signs will emerge at different points across the 2026/27 growing cycle. Australian wheat could face early-season precipitation deficits by late 2026, while rice systems in Southeast Asia may not begin to feel deficits until the 2027 monsoon season. Many staple crops in the Northern Hemisphere may be affected by the onset of ENSO in the late stages of crop growth and during harvest, but the greatest exposure will come during the 2027 growing season, when planting, pollination, and grain-fill periods align with peak El Niño conditions.

That creates a rare window for producers to adjust planting strategies, adopt more drought-resistant varieties, and secure irrigation inputs early. For upstream buyers, food manufacturers, and commodity traders, it also creates an opportunity to diversify supply, lock in contracts, and prepare contingency sourcing plans before disruptions intensify.

The window to act is not when the El Niño peaks. It’s now.

Governments in the most exposed countries already know this playbook. The Philippines has a dedicated El Niño Task Force. The FAO, which coordinates response plans across 34 affected countries, estimates that for every dollar spent on anticipatory action, farming families gain more than $7 in additional benefits and avoid losses.

Corporate teams rarely have anything equivalent to that level of preparedness: no task force, no pre-positioned contingency, no formal trigger for action. But these impacts will be felt across the agricultural value chain by both producers and their customers and will therefore require a concerted, planned effort.

Upstream buyers, food manufacturers, commodity traders, and ingredient sourcing teams should work with their supply chain to share information and limit exposure before price hikes are locked in and supplies are constrained. However, they should also consider hedging with suppliers in historically less-exposed regions.

If current trajectories hold, this could become the strongest El Niño event observed in modern records, surpassing even 1997 and 2015. The economic consequences of those events reshaped agricultural markets for years. Today’s supply chains are even more globally interconnected, climate-sensitive, and already overstretched due to geopolitics.

There is currently enough lead time for most producers and buyers to respond. The only advantage we have right now is time, and it’s running out faster than most procurement calendars assume.

The ESG News Editorial Team is comprised of veteran financial journalists and sustainability analysts dedicated to providing real-time, objective reporting on global ESG regulations, climate finance, and corporate governance. Our desk monitors daily developments from the SEC, IFRS, CSRD and international regulatory bodies to ensure our 1M+ readers receive accurate, data-driven insights into the evolving sustainable investment landscape. Follow the ESG News Editorial Team for expert reporting on global sustainability standards, ESG disclosures, and climate policy. Access over 10,000 investigative reports and real-time updates.